Role of the management accounting and treasury functions

The role of a management accountant is evolving as technology, globalisation and changing customer trends continue to impact on the business environment.

관리회계사들의 역할은 기술발전, 세계화, 고객들의 트렌드가 비즈니스환경에 영향을미치며 계속하여 발달하고있다.

Management accountants have traditionally focused on oversight and hindsight.

관리회계는 전통적으로 관리와 사후평가에 집중을 하였다.

Oversight ? 자원의 분배, 미래 투자를위해 재무가 탄탄한것을 확실히하는일 ..

hindsight? 사루평가..historical data를 이용해 미래의 프로젝트를 짠다.

또, 기업회계가 예전에는 원가회계 cost accounting , 예산짜는것 budgeting 에 신경을 더 썼다면 요새는 자동화가되고있는 매일매일의 operation 에서 더 높은 부가가치를 창출하는 전략적인 역할로 바뀌고있다.

The evolving responsibilities now include value creation, providing insight and foresight, and serving as strategically oriented business partners in an organisation.

이렇게 점점 발전되고있는 이 역할은 통찰력, 선경지명, 전략적임이 중요하다.

예를들어 전에는 descriptive, diagnostic 무엇이 일어났는지 서술하고, 왜 일어났는지 진단하는 역할이였다면 이제는 predictive, prescriptive and adaptive analysis 예측할수 있고 지시적이고 조정할수있는 분석을 할수있음이 중요하다

Differentiating management accounting from financial accounting

관리회계는 재무회계와 뭐가다른가 ??

간단히 정리해보면

관리회계> decision-makers들을 위한것, 기업안에서의 의사소통, 그렇기 때문에 회계기준이나 다른 외부의 룰들은 적용되지않음, 매니저와 다른 직원들의 행동에 영향을 주기위해 디자인됨.

재무회계>기업의 재무상태를 투자자,은행,규제 기관, 다른 외부의 단체와 의사소통을 하기위한것, 과거에 더 집중함 (과거에 일어난일을 분석하여 여태 어떻게 해왔는지 지금상태는 어떤지 알아야하기때문) , 외부와 소통하는것이기 때문에 회계기준, 회사법 등등이 적용됨, 데이타는 보통 회사의 회계시스템에서 얻음 !

Management accounting process

관리회계는 다섯가지의 스텝이 있다. !

1. Understanding the business information requirements of key stakeholders by clearly defining the issue

첫째, 아주 명확하게 이슈를 규정하며 주 stakeholder 들의 비즈니스 정보 요구를 이해하는것

2. Gathering the information necessary to produce a report that meets the business requirements.

둘째, 이 요구사항들을 이해했으면 정보를 모으자 !

3. Analysing and evaluating the information gathered.

셋째, 정보를 모았으니 분석하고 평가하자 !

4. Drawing conclusions based on anaylsis.

넷째, 이제 분석한것에 기반해 결론을 내자

5. Presenting information and making recommendations to management.

다섯째, 결론을 냈으니 정보를 전달하고 매니지먼트에 이제 어떻게 해야 좋을지 권고/제안한다.

하나하나 더 자세히 들여다보면..

1. Understanding the business information requirements of key stakeholders by clearly defining the issue

- A strong understanding of the organisation and its operations

stakeholder들과 효율적으로 의사소통 하기 위헤서는 기업과 운영에 대한 이해는 필수 필수 !!

- Good relationship with decision-makers and management

의사결정자들과 매니저먼트와 좋은 관계도 유지하자구요 !!

- An understanding of the different types of activities that management perform and the information required to support those activities

매니저먼트가 시행하는 다양한 활동들을 이해하고 필요한 정보를 챙겨 써포트를 하자

Strategic planning 전략플랜! 을 짜기위해 관리회계사로부터

- current financial position of the organisation

현재 기업의 재무상태

-Forecast of the future sales volumes, economic environment, costs and revenues

미래 쎄일즈에 대한 예측, 경제상황, 비용과 수익등등

-Competitor analysis

경쟁기업의 정보분석

-Customer analysis

고객분석 등등이 필요할것이다.

Operational analysis 작전분석 !

- current resources used and costs of operation

현재의 자원들이 어떻게 이용되는지 그리고 운영하는데에 비용은 얼마나드는지

-Future performance data

미래 퍼포먼스 데이타

-Senstivity analysis to show different outcomes depending on the approach taken

다양한 다른 방법에 따른 결과가 어떻게 다른지

등등이 필요할것이고..

Controlling and monitoring 감시 및 통제 프로세스를 위해선

-Performance levels compared to competitors

-Monthly operating results and analysis

-Sales/cost reports

-Cost analysis

.

.

.

등이 필요하다.

2. Gathering the information necessary to produce a report that meets the business requirements.

정보를 모으는것은 어떤 정보를 준비해야되냐 어떤 요청을 받았냐에 따라 다르겠지만 보통은

Internal data - 내부 데이타는 아이티시스템, 세일즈, 재무제표, risk reports, performance data, payroll data, compliance data, board papers

External data - 외부 데이타는 market, competitor and environmental analysis

3. Analysing and evaluating the information gathered.

비즈니스 문제를 해결하는데 있어 가장 중요한 분석과 평가 단계 ! 분석이란 그저 통계, 숫자들을 반복하는게 아닌 이 기업을 이해하고 분야 환경 등등 관련된것을 모두 이해하여 통찰력을 제공해야한다. 판단이 필요하며 다른 상호연결되어있는 부분들을 connect 할수 있어야한다.

IAS 37 Provisions, contingent liabilities and contingent assets prescribes the accounting and disclosure requirements for provisions and provides guidance on when and how to disclose contingent liabilities and contingent assets.

IAS 37 충당금, 우발 채무, 우발자산은 언제 어떻게 이 항목들을 기록해야 하는지 규정하고있다.

즉, 미래에 어떤 일이 일어날지 모르니 항상 비상금을 가지고있는 나의 텅장과 비슷하다고 보면 쉽다. 예를들어 언제 어떻게 어느 시점에 나갈지 모르는 내가 아플때의 병원비라던지.. 😊

All provisions have one thing in common: they are based on estimates of future cash flows, and, therefore, their measurement and recognition are subject to significant professional judgement.

모든 충당금은 미래의 현금 흐름에 기초해 있고 따라서 전문가의 판단이 아주 중요하다.

As a result, they are susceptible to over-optimism, over-cautiousness or error. Common problems that may arise with provisions include:

따라서 이 충당금,우발 채무, 우발 자산은 이 판단을 하는 데에 너무 낙관적이거나 너무 조심스럽거나 에러가 나타날 수 있다. 흔한 문제는 아래와 같다.

-Using provisions for profit smoothing 이익을 위해 충당금을 사용한다거나

(대변 또는 차변에 충당금을 넣고 이에따른 차변과 대변을 이익으로 기록하는 것 )

-Increasing provisions to cover any possible future liability

미래의 부채를 커버하기위해 충당금을 증가시킨다거나..

-Creating ‘big bath’ provisions – a term used to describe the practice of recognising certain expenses immediately.

Dr expense

Cr Provision

·Provisions

A provisional is defined as “a liability of uncertain timing or amount”.

충당금은 위에서 설명된 것과 같이 불확실한 부채이다. 예를 들면

-Warranty costs 워런티 (품질보증) 예를 들어 내가 전자사전을 샀는데 1년의 워런티가 포함되어있다. 이 워런티 기간에는 기계결함인 경우 수리를 받을 수 있다. 이때 이 전자사전 회사에게 이것을 고치기위해 든 비용은 warranty cost 가 된다.

-Decommissioning and restoration 해체,폐기처분 비용이나 복원비용

-Restructuring costs 리스트럭처링 비용 (기업 경영의 기본적 구조를 재구축하여 기업의 존속과 발전을 도모하기 위한 경영전략. 즉 사업의 개발,생산,유통 시스템을 변혁하고 재편성하여 발전 가능성이 있는 방향으로 가거나 비교우위가 있는 사업에 투자재원을 집중적으로 투입하는 경영 전략)

그럼 언제 충당금을 인지해야하는지 어떻게 알수 있을까?

Recognising provisions

A provision exists and must be recognised when all of the following criteria are met:

아래의 모든 것들이 충족될 때 충당금은 존재하며 반드시 인지되어야한다.

-An entity has a present obligation as a result of a past event

과거의 사건 으로 인해 현재의 의무가 있는경우

-It is probable that an outflow of resources embodying economic benefits will be required to settle the obligation

의무를 이행하기위해 경제적 자원 outflow 가 필요할 가능성이 있는경우

-A reliable estimate can be made of the amount of the obligation

이 의무에 관해 믿을 수 있을 만한 금액이 측정될 수 있는 경우

만약 이 조건들이 충족되지않는다면 충당금은 인식되지않는다.

Critical to the recognition of a provision is the requirement for there to be a present obligation.

충당금을 인지하는데에 있어서 가장 중요한 요소는 현재에 의무가 있냐는것이다.

A past event that leads to a present obligation is called an obligating event.

현재의 의무로 이끄는 과거의 사건 (계약 등등)을 “의무 발생 사건”이라고 부른다.

An obligating event is an event that creates a legal or constructive obligation, and therefore the entity has no realistic alternative to settling the obligation created by the event. This is the case only

의무발생사건은 법적의무 또는 의제의무를 발생시키고 따라서 기업은 이 사건에 의해 발생한 의무를 이행하는거 외에는 다른 방법이 없다. 예를들면

-Where the settlement of the obligation can be enforced by law

법적으로 집행될 수 있는 의무일경우

-In the case of a constructive obligation, where the event creates the valid expectations in other parties that the entity will discharge the obligation

기업이 특정책임을 부담한다는 것을 표명함으로써 그 책임을 이행할 것이라는 정당한 기대를 상대방이 가지게 되는 경우에 발생하는 의무

의제의무 의 예를 보면 아이폰을 판매한후 일정기간안에 기계의 결함이 있을 경우에 무상으로 수리를 해주거나 소모품의 일부를 무상으로 바꿔주는 약정이 포함되 있을 시에 회사는 언제 얼만큼의 비용이 누구에게 발생할지 불확실하더라도 금액을 추정해서 충당부채를 계산하여야 한다.

Distinguishing provisions from other liabilities

충당금을 다른 부채와 구분하기

Provisions can be distinguished from other liabilities due to the uncertainty concerning the timing or amount of the future expenditure require for their settlement.

충당금은 다른 부채와는 달리 시간적으로나 금액적으로 불확실하다

Measuring provisions

Having determined that a provision should be recognised, the next step is to measure it. In practice, this can be one of the most difficult and contentious areas of financial reporting for the entity.

이제 충당금이 인식되어야 된다는 걸 알았으니 어떻게 측정하고 리포팅을 하느냐가 관건인데 기업에게는 이부분이 아주 어렵고 논쟁이 많이 벌어지는 부분이다.

The amount recognised must be the best estimate of the expenditure required to settle present obligations at the reporting date, taking into account the risks and uncertainties that surround the events and circumstances affecting the provision. It should reflect the amount that an entity would rationally be required to pay to settle the obligation at the reporting date, or to transfer to a third party at time.

The amount of the provision is estimated using the judgement of management, supplemented by experience of similar transactions and, in some cases, reports from independent experts. Events after the reporting date should also be considered.

If settlement is expected to occur after more than one year, and the effect of the time value of money is material, the amount should be discounted using a pre-tax rate specific to the liability. The discount rate is not adjusted for risk that have already been taken into account in the cash flow estiamtes.

At each reporting date, the provision needs to be remeasured and adjusted to reflect the current best estimate.

리포팅 날마다, 충당금은 다시 계산 되어야하고 현재의 제일 적합한 예측을 반영할수 있어야 한다.

If the provision is measured using discounted cash flows, the carrying amount of the provision will increase each year to reflect the passage of time and, hence, the unwinding of the discount. This increase is recognised as a borrowing cost and treated as an expense.

만약 이 충당금이 할인현금수입가치 를 이용해 계산이 되었다면, 충당금의 장부가액은 시간의 흐름을 반영하기 위해 매년 증가할 것이다. 이 증가는 차입원가로 인식되고 비용처리된다.

(할인현금수입가치 : 미래현금흐름기대치를 해당 현금이 갖는 위험수준 반영의 율(rate)로 할인한 값으로써 기업의 가치를 평가하는 방법이다. 앞으로 발생할 이익을 모두현재가치로 환산해자산가치를 평가한다. 일반적으로 이익발생기간은 10년으로 잡는 경우가 대부분이다)

Applying recognition and measurement rules

IAS 37 provides guidance on how to apply the recognition and measurement rules for specific matters.

IAS 37은 특별한 상황에 어떻게 인지하고 계산해야 하는지 알려준다.

Future operating losses

미래의 영업손실

Provisions shall not be recognised for future operating losses as the entity does not have a present obligation as a result of a past event.

충당금을 인지하기 위해서는 세가지의 조건이 필요했다 그 중에 제일 중요했던 현재의 의무가 있냐 없냐!?

미래의 영업손실은 과거의 이벤트로 인해 발생하는 현재의 의무가 없기 때문에 충당금으로 인식될 수 없다.

Onerous contracts

유상계약

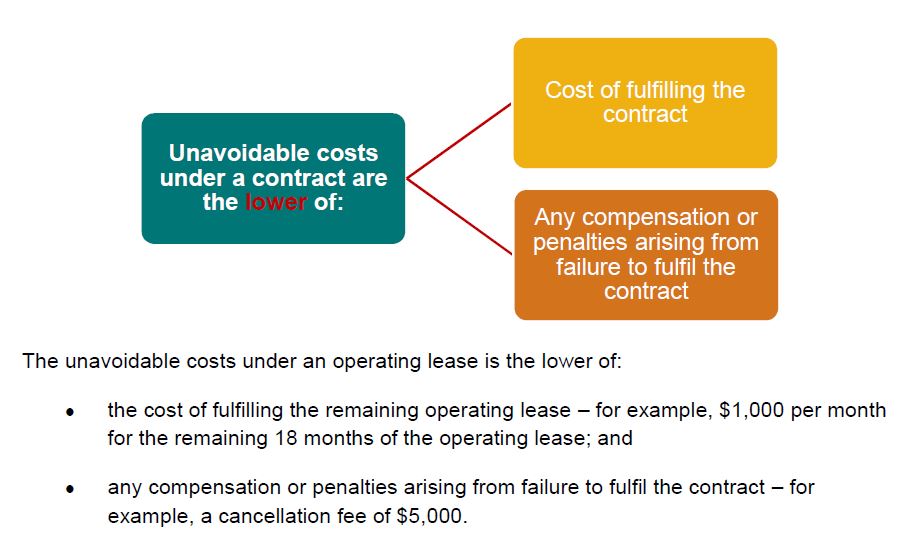

An onerous contract is a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

유상계약이란 경제적 가치보다 이 의무를 이행 하는데 에 있어서 드는 불가피한 금액이 클 때이다.

An onerous contract meets the three criteria for recognising a provision and, therefore, a provision should be recognised for the unavoidable costs under the contract. The unavoidable costs reflect the least net cost of exiting the contract, which is the lower of the cost of fulfilling it and any compensation or penalties arising from failure to fulfil it.

유상계약은 충당금을 인식하는 데에 있어서 세가지 요소에 들어맞기 때문에 이 불가피한 비용에 대해 충당금이 인식해줘야 하고 이 불가피한 비용은 계약을 종료하는 데에 드는 최소 순비용을 반영하고, 이는 계약을 이행해야할때 드는 비용과 이행하지 않았을 때 발생하는 계약 이행 실패 벌금 중 낮은 금액이다.

Onerous contracts, including onerous executory contracts, are accounted for in accordance with AASB 137: Provisions, Contingent Liabilities and Contingent Assets. Executory contracts are contracts under which neither party has performed any of its obligations or both parties have partially performed their obligations to an equal extent. Typical examples of executory contracts include:

계약을 맺은 두 그룹이 아무도 의무를 이행하지않았거나 둘다 그들의 의무를 같은범위안에서 의무를 이행했을때 예를들어보면

Operating leases of floor space (tenant has to make periodic rental payments/landlord has to provide accommodation);

내가 사업을 하려고 빌딩의 한 오피스를 운용리스로 빌렸다. 그렇다면 나는 그 기간동안 렌트비를 내야하고 이 빌딩읫 소유주는 이 장소를 제공해야만 한다.

Operating leases of equipment (lessee has to pay operating lease instalments/lessor has to provide equipment for use by the lessee)

사무실에서 쓰려고 아주 큰 프린터를 운용리스로 빌렸다 그렇다면 나는 이에 해당하는 비용을 할부로 내거나 스케줄에따라 지불을 해야하며 Lessor (빌려준사람 - 임대인) 은 이 프린터를 제공해야만한다.

Development contracts (development work required/payment required when milestones achieved); and

신제품을 개발하는데 중요한 단계가 지나면/다다르면 돈을 지불해야한다

예를들어 남은 사무실 임대의 기간이 18개월동안 한달에 $1,000 불씩나간다 치자

만약 이 계약을 깨버리면 계약파기비용으로 $5,000 불을 내야한다 이경우에 unavoidable costs 불가피한 금액은

$5,000 이 된다 ( $1000 *18 = $18,000) 둘중 더 낮은금액이 되야하기때문.

글로벌위기때는 자산의감소를 인지하는데 좀 느렸다. 이유는 금융자산과 마찬가지로 전에는 발생한후에만 인지를 하였기 때문이다. 다시한번 강조하는 IFRS 9 은 Forward-looking !! 앞을보는것 미래의손실까지 예측하는것 !! 준비된자만이 위기를 극복할수있다.

IFRS 9 anticipates that credit losses will be recognised prior to a financial asset becoming credit-impaired or an actual default occurring.

그렇다면 이 자산의 감소/경제적 가치가 손상되었다는것은 무슨말일까 ?

A credit loss occurs when an entity receives lower cash flows than the amount that is contractually due to it.

받기로했던 돈보다 적게 받을수밖에없는상황이 되었을 때 우리는 그 떨어진 가치를 어떻게 기록해야하는가에 대한 문제이다.

IFRS 9 은 기업이 아래의 손실들을 재무상태표 (the statement of financial position /balance sheet)에 기록하도록 한다.

FRS 9 requires an entity to recognise a loss allowance in the statement of financial position for expected credit losses on

-Financial assets measured at amortised cost or FVTOCI

-Lease receivables

-Contract assets

-Loan commitments that are not measured at FVTPL

-Financial guarantee contracts that are not measured at FVTPL

This means that a loss allowance is not recognised for

-Financial assets measured at FVTPL

-Equity instruments measured at FVTOCI

위의 조건들은 언제든지 참고해서볼수있으니 외우는데 열중하지말고 예시/실제상황이 왔을 때 어떻게 대입하냐가 중요하다

그렇다면 어떻게 이걸 예측할수있을까 ?

-The period over which to estimate expected credit losses (ECLs). Entities must consider the maximum contractual period over which the entitiy is exposed to risk, including extension options exercisable by the borrower, the term of contractual commitment under financial guarantees, and undrawn loan commitments.

-Unbiased probability-weighted outcomes.

-The time value of money. Expected cash flows are discounted to the reporting date using the effective interest rate determined at initial recognition, or the current effective interest rate if the financial asse has a variable interest rate.

-Reasonable and supportable information.

-Collateral (담보물)

한마디로..모~~든 가능성을 염두해라 !

예를들어 A회사가 매출채권에관해 아래와같은 historical자료를 가지고있다

Not past due 1%

0-3 days past due 2%

31-90 days past due 5%

91-180 days past due 15%

>180 days past due 25%

모든 손님들은 같은지역사람들이며 경제적타격이나 조건들이 비슷하다고한다

이 회사는 현재와 미래의 경제조건들을 예측했을 때 큰변화가 없을거라고 판단한다. 그렇다면 이회사는 이 자료를 credit loss를 예측하는데 쓸것이다.

IFRS 9을 적용하는데 있어서 기업들은 아래중 해당되는상황에따라 쓸수있다

-The general approach – applied to most loans and debt securities

-The simplified approach – applied to most trade receivables

-The purchased or originated credit-impaired approach

-Low credit risk operational simplification

하나하나 자세하게 살펴봐볼까 ?

1.The general approach

-No loss allowance for expected credit losses recognised as the asset is initially recognised at fair value.

@ Each reporting date

-Stage 1: If there is no significant increase in credit risk since initial recognition, entities provide for expected credit losses that may result from default events possible within the next 12 months.

처음 기록후에 큰 변화가 없다면 12개월안에 일어날 변화들에 대한 것을 제공한다. 반대로 첫 recognition 이후로

2.The simplified approach to impairment

-It doesn’t require the tracking of changes in credit risk, but instead requires the recognition of lifetime ECLs at all times.

여기서 중요한 포인트 ~~

Trade receivable과 contract asset은 어차피 12개월안에 만료라는 것 그래서 12개월 ECL과 같다 !

3.Purchase of originated credit-impaired approach

Detrimental impact on the estimated future cash flow

예시로는 아래와 같다.

-Significant financial difficulty of the issuer or borrower

-A breach of contract

-The lender has granted to the borrower a concession

-Borrower will enter bankruptcy

-The disappearance of an active market

4.Low credit risk operational simplification

-A financial asset that is determined to have low credit risk

IFRS 9 indicates that a financial asset is considered to have low credit risk if

-There is a low risk of default by the borrower

-The borrower has a strong capacity to meet its contractual cash flow obligations in the near term

-Adverse changes in economic and business conditions in the longer term may, but not necessarily, reduce the ability of the borrower to fulfil its contractual cash flow obligations.

-A financial liability or equity instrument가 있어야 한다.

그럼 하나하나 자세히 살펴보자

A financial asset– is a contractual right arising from a past transaction that provides future economic benefit to an entity and a result in a financial liability or equity of another entity.

A financial asset 이란 과거의 거래로 인해 발생하는 계약상의 권리이며 한회사에는 경제적 이익을 가져다 줄 것이고 따라서 다른 회사에는 liability 나 equity 가 발생할 것이다.

예를들어 종류는 ?

Financial asset

-현금 ! 돈 ! (은행계좌)

-Trade receivables 이나 investments in bonds 채권투자 or convertible notes 컨버터블 노트 [우선 투자하고 향후 성과가 나왔을 때 전환가격을 결정하는 오픈형 전환사채]

-Equity share

-Contractual right to exchange financial instruments under potentially favourable conditions. [조건이 좋을때만 이 회사가 exercise할 CALL option이나 PUT option]

Financial liability는 financial asset의 완전반대의 개념!

A financial liability is a type of contractual obligations arising from a past event that is expected to result in an outflow of economic benefits and results in a financial asset of another entity.

예를들어 종류는 ?

Financial liability

-Trade payables . borrowings, financial guarantees or issuance of bonds

-콜옵션이나 풋옵션 (다른 회사들이 컨디션이좋을 때 exercise할것이니 나에게는 컨디션이안좋을때가 되겠죠)

Equity instrument는 ?

An equity instruments is any contract that evidences a residual interest in the asset of an entity after deducting all of its liabilities. Share issued by a company will be an equity instrument of that company.

쉽게말해 자산에서 모든부채를 차감한후의 잔여지분을 나타내는 모든계약이다 – 회사가 주식을 발행했다면 이는 이 회사의 equity instrument가 되는것이다. 😊

Equity instrument 예시를 봐보자 !

2020년 11월 1일에 S 회사가 1 million 보통주를 $ 2 million 에 발행하였다. 이때 $200,000 의 발행비용이 발생하였으며 2020년 12월 31일에 S 회사는 주식 당 배당을 15c 에 선언하였고 이는 2021년 3월 15일에 지급 되어야 한다.

2020년 11월 1일

DR

CR

Cash at bank

2,000,000

Ordinary share capital

2,000,000

2020년 11월 1일

DR

CR

Ordinary share capital

200,000

Cash at bank

200,000

(발행비용)

2020년 12월 31일

DR

CR

Dividend paid

150,000

Dividend payable

150,000

(1 million share x 0.15c declared)

2021년 3월 15일

DR

CR

Dividend payable

150,000

Cash at bank

150,000

😊오늘의 학습 복습 !😊

- IFRS 9 은 미래 대손충당금까지 반영하는 forward-looking 이라는것

Financial instruments

- 한쪽에는 financial asset이되고 다른쪽에는 financial liabilit 또는 equity instrument가 된다.

Financial asset 의 예시

- trade receivables, investment in bonds or convertible notes

Financial liability의 예시

- trade payables, borrowings, financial guarantees or issurance of bonds